Can You Sell Your Mortgaged Home in Dubai? Yes, and Here’s How It Works

You can sell a mortgaged home in Dubai. It happens every day, and the process is well established. The outstanding loan on your property does not prevent a sale. It simply adds a few steps that need to be handled in the right order. A large share of the sellers we work with are upgrading to a bigger property, and they come to us worried that having a mortgage makes the whole thing too complicated to manage. The process is very manageable once you understand how the pieces fit together.

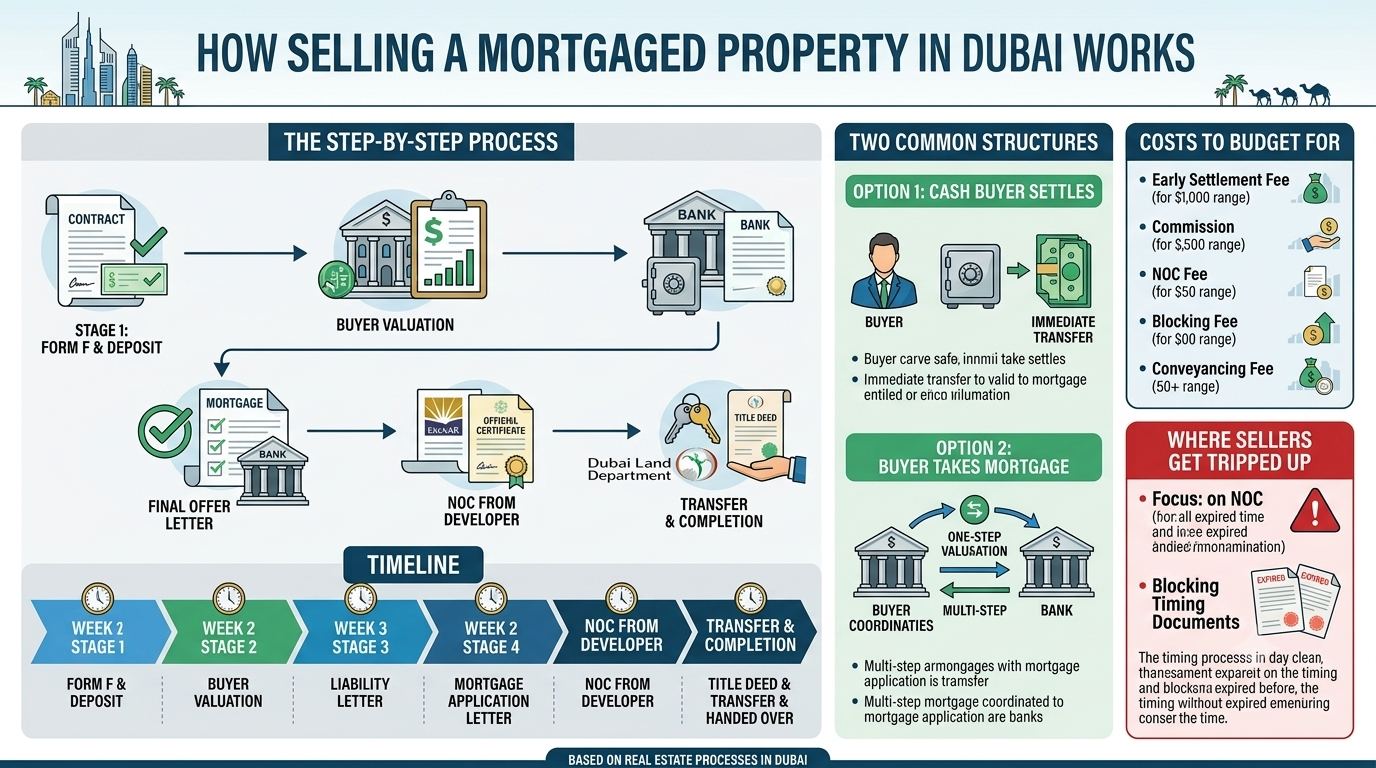

This guide walks through exactly how a mortgaged property sale works in Dubai, what it costs, how long it takes, and the part of the process that catches most sellers off guard.

How Selling a Mortgaged Property Works

When you have a mortgage on your Dubai property, your bank holds the title deed until the loan is repaid. To sell, the outstanding loan has to be cleared so the title can be transferred to the buyer free of any charge against it. There are two common ways this gets structured, and the right one depends on your buyer.

Option 1: Cash Buyer Settles the Loan First

This is the most straightforward route and the one we see most often. The buyer pays off your outstanding mortgage directly to your bank, your bank releases the title deed, and the property then transfers to the buyer at the Dubai Land Department. The buyer’s settlement of your loan counts toward the purchase price, and they pay you the balance. Because there’s only one bank involved, this version moves faster and has fewer moving parts.

Option 2: Buyer Takes Their Own Mortgage

When the buyer is also financing their purchase, two banks are involved. The buyer’s bank settles your outstanding loan, your bank releases the title, and the buyer’s bank registers its own mortgage against the property at transfer. This works smoothly but takes longer because the two banks need to coordinate, and the buyer’s financing has to be fully approved before anything can complete.

The Step-by-Step Process

Here is how a mortgaged sale progresses from listing to completed transfer.

Sign Form F and Pay the Deposit

Once you’ve agreed terms with a buyer, both parties sign Form F, the unified sale contract registered through the Dubai Land Department. The buyer typically pays a 10% deposit at this stage, usually held by the agent or a conveyancer.

Buyer’s Valuation

If the buyer is financing, their bank orders a valuation of the property to confirm it’s worth the agreed price. This takes around 3 to 5 working days.

Request Your Liability Letter

You request an official Liability Letter from your bank, which states the exact amount remaining on your mortgage. This letter is what allows the sale to be priced and settled correctly, and it usually takes 7 to 10 working days to be issued.

Buyer’s Final Offer Letter

If the buyer is using a mortgage, their bank reviews your Liability Letter and issues its Final Offer Letter, confirming it will fund the purchase.

Obtain the NOC from the Developer

Before any transfer can happen, the developer, whether that’s Emaar, DAMAC, Nakheel, or another, issues a No Objection Certificate confirming you owe no outstanding service charges. This step takes anywhere from 3 to 7 working days, and it’s the one that most often holds things up. More on that below.

Mortgage Clearance and Final Transfer

The buyer’s bank prepares settlement cheques to clear your mortgage. Once your bank confirms receipt and releases the title deed, both parties attend a DLD Registration Trustee office to block, transfer, and register the property under the new owner’s name.

How Long Does It Take?

A standard mortgaged sale typically takes around 6 to 8 weeks from signing Form F to final transfer. Here is roughly how that breaks down:

| Stage | Timeframe |

|---|---|

| Pre-approval and valuation | Weeks 1 to 2 |

| Liability Letter and Final Offer | Weeks 3 to 4 |

| NOC from developer | Weeks 5 to 6 |

| Mortgage clearance and transfer | Weeks 7 to 8 |

If both you and your buyer have active mortgages with different banks, what’s known as a mortgage-to-mortgage deal, the timeline can extend toward 8 to 12 weeks, because there are twice the administrative layers to clear.

The Part That Trips Sellers Up: NOC and Blocking Timing

In our experience, the stage that causes the most frustration is the timing around the NOC and the blocking of the property. Sellers often assume the transfer can happen as soon as a buyer is ready, but the developer’s NOC has to be in hand first, and that can take up to a week or more depending on the developer. If there are any unpaid service charges, even small ones you’d forgotten about, the NOC won’t be issued until they’re cleared, which adds further delay.

The blocking step also catches people out. Blocking is a DLD mechanism that temporarily freezes the property so the buyer’s bank can release funds with the security of knowing the title can’t be transferred to anyone else in the meantime. Coordinating the blocking, the loan settlement, and the title release to all line up on the same day takes organisation, and it’s where a good agent and conveyancer earn their fee. Getting these steps sequenced correctly is the single biggest factor in whether your sale completes in six weeks or drags toward twelve.

What It Costs to Sell a Mortgaged Property

Selling a mortgaged property carries the standard selling costs plus a few specific to having a loan. Budget for the following:

| Cost | Typical Amount |

|---|---|

| Early settlement fee (charged by your bank) | 1% of outstanding loan, capped at AED 10,000 |

| Agency commission | 2% of sale price plus VAT |

| NOC fee (developer) | AED 500 to AED 5,000 depending on developer |

| DLD blocking fee | Approximately AED 1,500 |

| Conveyancing fee (optional but recommended) | AED 5,000 to AED 10,000 |

The early settlement fee is the one sellers most often forget to factor in. UAE Central Bank rules cap it at 1% of your outstanding balance or AED 10,000, whichever is lower, so it rarely becomes a large number, but it’s worth knowing about before you do your sums.

Will a Buyer Want a Mortgaged Property?

A mortgage on your property makes no difference to most buyers. From their side, they’re buying a home, and the existence of your loan is a back-office matter handled between the banks and the DLD. Cash buyers settle the loan as part of their purchase, and mortgage buyers have their bank handle it. The property transfers to them with a clean title either way, so there’s nothing for them to inherit or worry about.

If anything, a mortgaged property signals to a buyer that the home has already passed a bank’s valuation and due diligence at some point, which can offer a degree of reassurance.

Tips for a Smooth Mortgaged Sale

A few things that make the process easier, based on the sales we handle:

Request your Liability Letter early. It takes up to 10 working days, so getting it moving as soon as you have a serious buyer saves time later.

Clear any outstanding service charges before you list. This prevents the NOC from being held up when you’re ready to transfer.

Use a conveyancer if your sale involves two banks. The coordination between lenders is where deals slow down, and having someone manage that sequencing properly is worth the fee.

Be realistic with your buyer about timing. If they expect to complete in three weeks, set expectations early that a mortgaged sale realistically takes six to eight.

Frequently Asked Questions

Can you sell a mortgaged property in Dubai?

Yes. You can sell a property in Dubai that still has an outstanding mortgage. The loan is settled as part of the sale, either by a cash buyer paying it off directly or by the buyer’s bank clearing it before the title transfers. The process is routine and handled through the Dubai Land Department.

How long does it take to sell a mortgaged home in Dubai?

A standard mortgaged sale typically takes around 6 to 8 weeks from signing Form F to completing the transfer. If both buyer and seller have active mortgages with different banks, it can extend to 8 to 12 weeks because of the additional coordination required between lenders.

What is the early settlement fee on a Dubai mortgage?

UAE Central Bank rules cap the early settlement fee at 1% of your outstanding loan balance or AED 10,000, whichever is lower. This is charged by your bank for paying off the loan ahead of its term, and it’s a cost sellers should factor in before listing.

What is an NOC and why do I need one to sell?

An NOC, or No Objection Certificate, is a document issued by your property’s developer confirming you have no outstanding service charges or dues. It’s required before any property transfer can take place at the Dubai Land Department. If you have unpaid service charges, the NOC will not be issued until they’re cleared.

Can I sell my mortgaged property to a buyer who also needs a mortgage?

Yes. This is known as a mortgage-to-mortgage sale. The buyer’s bank settles your outstanding loan and then registers its own mortgage against the property at transfer. It works smoothly but takes longer than a cash sale because two banks need to coordinate, typically pushing the timeline toward 8 to 12 weeks.

Do I need to pay off my mortgage before listing my property?

No. You don’t need to settle your mortgage before putting your property on the market. The loan is cleared during the sale process itself, using the proceeds from the buyer. Settling it yourself beforehand is an option, though it ties up your own capital unnecessarily for no real benefit.

Thinking of Selling Your Mortgaged Home?

Selling a mortgaged property in Dubai is a well-trodden path, and with the right sequencing it completes in around six to eight weeks. If you’re upgrading, relocating, or simply ready for a change, the mortgage on your current home is no barrier to moving forward. Speak with our team and we’ll walk you through the process and manage the bank coordination so the sale runs as smoothly as possible.